Estonia’s financial regulator, Finantsinspektsioon, announced on March 26 that the European Central Bank (ECB), acting at Estonia’s request, had revoked the license of Versobank AS, a small Estonian bank catering to clients based in Russia and Ukraine. According to Finantsinspektsioon, the license was withdrawn for “serious and long-lasting breaches of legal requirements, particularly concerning the prevention of money laundering.” With this action, Estonia continues to demonstrate that it has no desire to serve as a hub for illicit Russian financial activity, which is part of the asymmetric toolkit the Russian government uses to undermine democratic institutions across the transatlantic space. And, for the first time, the ECB has now taken explicit, unequivocal action to shut down a bank for money laundering violations. This precedent gives the ECB and European national regulatory authorities a new and powerful tool to combat Russian illicit financial activity in Europe. The more aggressive stance also augurs well for enhanced U.S.–EU cooperation.

Estonia Tightens the Reins

Following a series of Russian and other money laundering scandals at the Estonian branch of Denmark’s Danske Bank that came to a head in 2014, Estonia moved quickly to reduce the amount of non-resident accounts in the banking system, thereby lowering the risk of money laundering through opaque foreign shell companies. Finantsinspektsioon oversaw a reduction in foreign deposits from a 2014 peak of 20 percent to 14 percent in late 2016, down to 10 percent by late 2017.

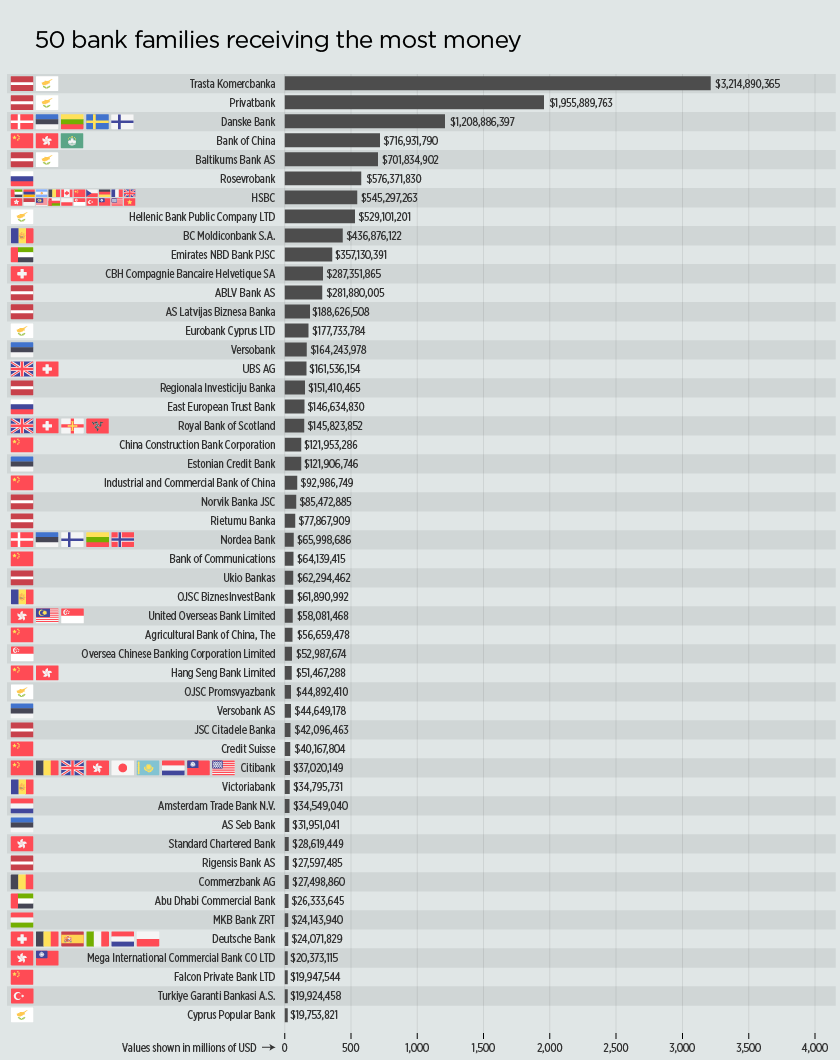

Versobank has been involved in a variety of money laundering schemes, including the infamous “Russian Laundromat” in Moldova that has been brilliantly covered by the Organized Crime and Corruption Reporting Project. The Laundromat moved approximately $20 billion out of Russia, primarily through the following route: companies banking at Moldinconbank in Moldova held fake “debts,” which were “paid” by Russian companies moving money out of Russia on behalf of a variety of Russian clients, including wealthy, politically connected businesspeople. The money would be wired from Moldinconbank to Trasta Komercbanka in Latvia and, from there, across the globe. Versobank accounts reportedly received $200 million related to the scheme. After a series of four onsite inspections and proposed remediation, Finantsinspektsioon grew disillusioned with Versobank’s prospects for reform. It submitted its recommendation to the ECB in February. With its post-Danske reduction in the non-resident banking sector and its successful proposal to the ECB to revoke Versobank’s license, Estonia has delivered a clear message to those facilitating illicit Russian financial activity — Estonia is closed for business.

The ECB Begins to Focus on Money Laundering

Under the ECB’s Single Supervisory Mechanism, established in 2014 in response to the eurozone crisis, the ECB possesses the sole authority to grant or withdraw a banking license, not the financial regulators of participating European Union member states. The ECB is also responsible for direct “prudential” supervision of banks that have been determined to be “significant entities” on the basis of their size and systemic importance (“prudential” supervision refers to monitoring of things like capital adequacy and lending practices). Prudential supervision of “less significant institutions” is delegated to national competent authorities. At the same time, supervision of compliance with anti-money laundering requirements at banks of all sizes is the responsibility of national regulators. Thus, the ECB has had limited insight into any illicit financial activity occurring at European banks or the risks of such incidences occurring owing to inadequate controls. And, until Versobank, the ECB had never pulled a license on the explicit grounds of money laundering violations.

The new, aggressive tone on money laundering from the ECB is a positive shift from past practice. For example, in March 2016, Latvia’s financial regulator, the Financial and Capital Market Commission, announced that the ECB had withdrawn the license of the aforementioned Trasta Komercbanka. Like Versobank, Trasta had been involved in a number of Russian and other money laundering scandals. But when the ECB pulled Trasta’s license, the stated basis was primarily “prudential” concerns. This time around, in a first for the ECB, Versobank was called out for repeated, egregious anti-money laundering violations, which were the centerpiece of the ECB’s action. The ECB also allowed Finansinspekstioon to publish the ECB’s decision, which details Versobank’s money laundering failings and specifically notes the nexus with Russia.

ABLV in the Background

The ECB’s decisive action against Versobank comes just weeks after the targeting in February of Latvia’s ABLV Bank by the U.S. Treasury Department under Section 311 of the USA PATRIOT Act. ABLV, which is currently undergoing ECB-ordered liquidation following the Treasury action, was the leading bank in Latvia catering to non-resident customers. The Treasury Department found that ABLV had “institutionalized money laundering as a pillar of the bank’s business practices” and facilitated “large-scale illicit activity connected to Azerbaijan, Russia, and Ukraine.” Latvia has developed a far more extensive non-resident banking sector than Estonia, with about a dozen banks catering to non-resident money, most of it emanating from Russia and other countries of the Commonwealth of Independent States. Non-resident deposits in Latvia’s banking system reached a peak of over 50 percent and are currently below 40 percent, although the government has recently vowed to bring the number down to a manageable 5 percent.

Transatlantic Cooperation on Illicit Finance

Recent developments in Latvia and Malta – as well as longstanding issues in Cyprus – have started a much-needed discussion about whether money laundering supervision in Europe should be entrusted to a central authority with greater resources and capacity than the national authorities of smaller European states. Such a central authority could also proactively revoke or restrict licenses without needing to wait for national authorities to submit a recommendation. This policy discussion presents an opportunity to evaluate which national regulators need to be further strengthened, how to deepen European information-sharing to combat illicit financial activity, and whether there needs to be a more assertive role for European law enforcement in combating Russian money laundering. This week’s coordinated action by Estonia and the ECB is a welcome step in the right direction and may presage greater intra-European cooperation and, potentially, the emergence of a coordinated transatlantic response to Russian illicit finance.

The views expressed in GMF publications and commentary are the views of the author alone.

{kind=link}